Public debt is not inherently a problem. In fact, every modern economy borrows. Governments issue debt to finance highways, railways, schools, hospitals, defense, and other investments that would be difficult to fund through annual tax revenues alone. When used wisely, borrowing allows a nation to accelerate development and improve the quality of life for its citizens.

The challenge begins when debt grows faster than the economy can support.

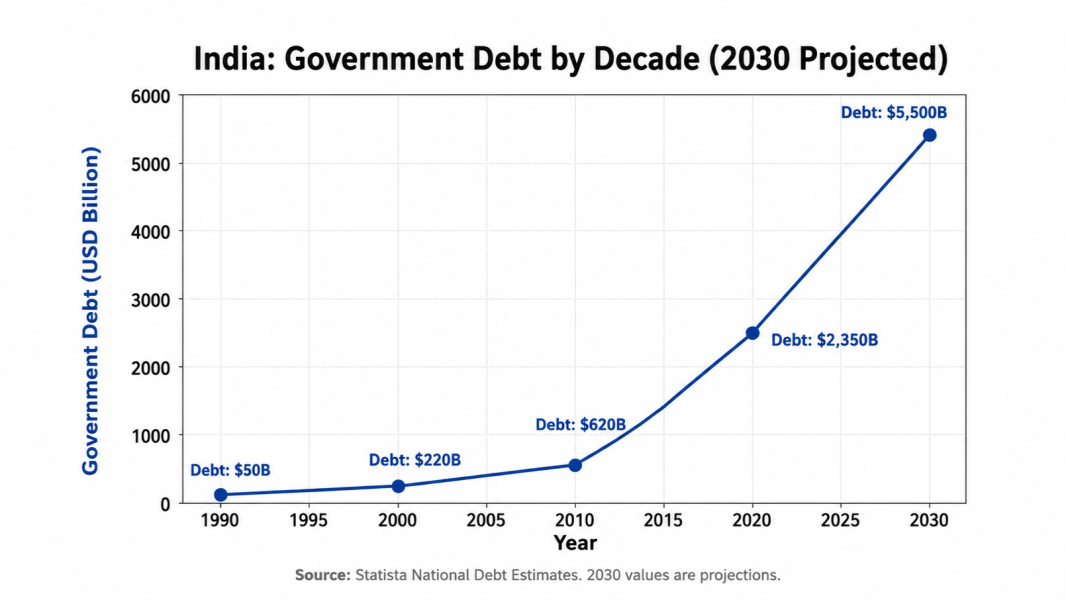

India has made remarkable progress over the past three decades. Millions have escaped poverty, infrastructure has expanded rapidly, and the country’s economy has become one of the world’s largest. These achievements required significant public investment, and borrowing has played an important role in financing that transformation.

However, rising public debt deserves careful attention—not because borrowing is inherently harmful, but because it creates long-term obligations that future taxpayers must ultimately bear.

Every rupee borrowed today must eventually be repaid or refinanced. Interest payments consume government revenues that could otherwise be invested in education, healthcare, scientific research, public safety, or tax relief. As debt grows, these interest costs become an increasingly large part of government expenditure, reducing fiscal flexibility during future economic downturns or national emergencies.

This raises an important question: Are we borrowing primarily to create productive assets that generate future economic growth, or to finance current consumption and recurring expenditures?

The distinction matters.

When borrowed funds finance high-quality infrastructure, improve education, strengthen healthcare systems, modernize logistics, or enhance productivity, they create economic returns that help future generations repay today’s borrowing. These investments expand the economy’s productive capacity and increase future tax revenues.

On the other hand, borrowing that primarily finances recurring expenditures without improving productivity leaves future citizens with larger repayment obligations but few additional assets to support them.

India’s long-term prosperity cannot depend indefinitely on expanding public debt. Sustainable economic growth requires a broader foundation.

First, institutions must continue to become more efficient and accountable so that public spending delivers measurable outcomes. Every borrowed rupee should create visible economic value.

Second, investment must increasingly flow toward sectors that improve productivity, generate employment, and expand exports. Productive investment strengthens the economy’s ability to service debt without placing excessive pressure on taxpayers.

Third, India needs a broader and more efficient tax base. A larger formal economy distributes the burden of public finance across more citizens and businesses while allowing tax rates to remain competitive.

Finally, fiscal discipline remains essential. Governments must balance today’s development needs with tomorrow’s financial stability. Borrowing should complement economic growth—not substitute for it.

History offers many examples of countries that used debt effectively to accelerate development. It also offers cautionary examples in which excessive borrowing limited future policy choices, slowed growth, and shifted significant financial burdens onto younger generations.

India has the opportunity to follow the first path.

The country’s demographics, entrepreneurial talent, expanding manufacturing base, digital infrastructure, and growing global influence provide a strong foundation for long-term growth. If public borrowing is matched by productivity gains, institutional reform, and disciplined fiscal management, debt can remain a valuable tool rather than becoming a constraint.

Economic policy should therefore focus not simply on how much the government borrows, but on how effectively those borrowed resources are invested and whether they strengthen the nation’s long-term productive capacity.

Debt is ultimately a promise made by the present to the future. Honoring that promise requires more than repayment—it requires ensuring that future generations inherit an economy stronger than the one that incurred the debt.

A nation cannot build lasting prosperity through debt expansion alone. Lasting prosperity is built through productive investment, strong institutions, responsible fiscal management, and sustained economic growth. Debt may help finance the journey, but productivity and discipline determine the destination.

Leave a Reply